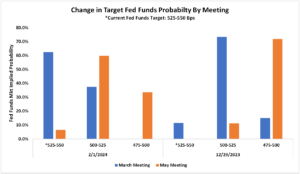

There’s something happening here, but what it is ain’t exactly clear. The late, great Buffalo Springfield could have been describing the markets because action last week was indeed very curious. Overall, the week was dominated by commentary from the Federal Reserve following their decision to leave interest rates unchanged, as was widely expected. In addition, labor-related data continued to show a tight labor market as a result of a U.S. economy that continues to “punch above its weight.” But before we stop, children what’s that sound… Commentary from Jerome Powell following the release of the Fed’s stance essentially dashed most of the hope for a March interest rate cut given the continued strength in the economy as well as the persistence of inflation running above target. As expected, the probability of an interest rate cut in March dropped to 30% from 90% at the end of last year (see chart of the week below). But honestly, it was the market action following Powell’s comments that was most intriguing and potentially indicated a shift in the market backdrop going forward. Despite an initial sell-off, equity markets have largely held on to recent gains while the yield on the 10-year note has dropped by roughly 30 basis points to 3.85%. The combined action of stocks and bonds, following a shift in the landscape of monetary policy, hints at an equivalent shift in market narrative away from purely policy-driven markets to a renewed focus on the strength of the underlying economy and corporate earnings growth. The breadth of the equity market action helps support the thesis with cyclical oriented stocks, as well as small caps, participating in the market recovery late last week. It just may be that investors are passing the baton from monetary policy back to fundamentals. And with that passing of the baton will be a renewed focus on fundamentals and strength of the underlying economy and away from speculation and decoding of fed commentary. I guess Buffalo Springfield was right, “Paranoia strikes deep. Into your life it will creep.”

1. Interest Rates Unchanged – Both the Federal Reserve and the Bank of England kept interest rates unchanged while offering commentary that interest rate cuts would be further into the future than market expectations. 2. U.S. Job Openings – Job openings nationally came in at 9 million versus estimates of 8.75 million, while total separations, which include “quits,” declined from November’s reading. 3. Tech Earnings – Amazon, Meta, and Apple all reported solid revenue. Concerns over slowing demand for Apple were overshadowed by positive reactions to Amazon and Meta’s earnings, with both stocks up after reporting.

Monday · Eurozone Services PMI · U.K. Services PMI · Eurozone Producer Prices · S&P U.S. Services PMI · ISM Non-Manufacturing PMI Tuesday · Eurozone Retail Sales Wednesday · German Industrial Production · U.S. Consumer Credit · Chinese CPI Thursday · U.S. Initial Jobless Claims Friday · German Inflation

Drop in Probability of Interest Rate Cut in March 2024 Since End of 2023

|